What Is a Balloon Mortgage Miami Homebuyer Guide

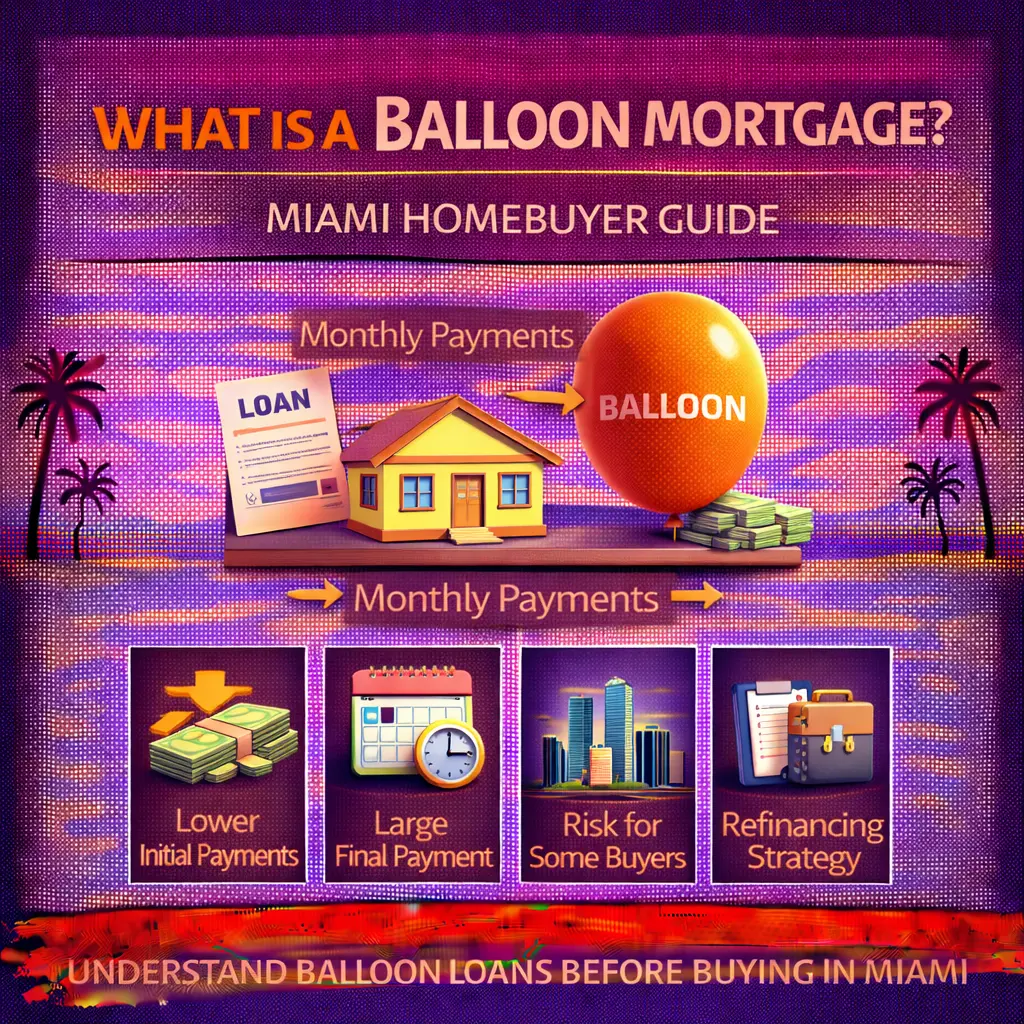

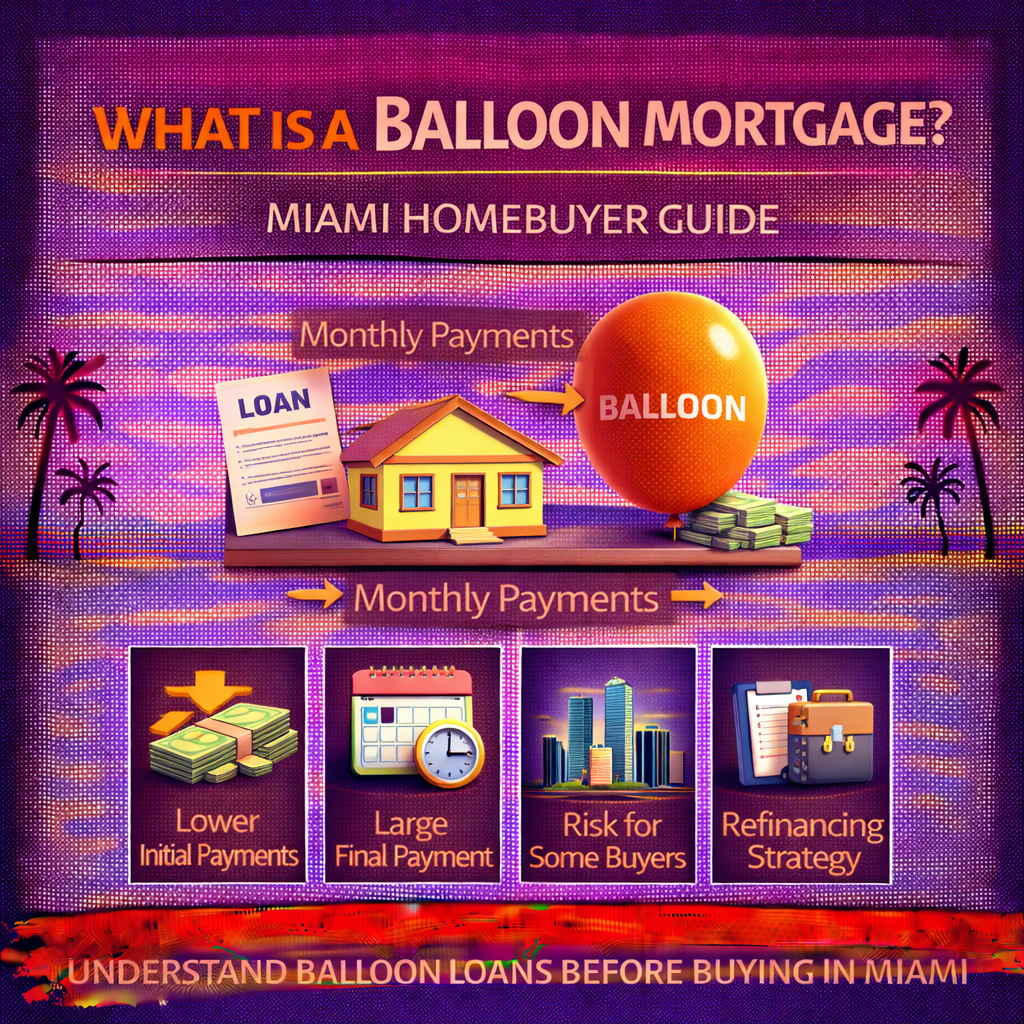

What Is a Balloon Mortgage?

Discover what a balloon mortgage is, how it works, risks and benefits, and whether it fits your plans when buying a home in Miami neighborhoods like Coral Gables, Coconut Grove, and Miami Beach.

Introduction: Mortgage Options in Miami

When shopping for real estate in Miami — whether a luxury condo near Miami Beach, a family home in Coconut Grove, or a newly built townhome in Doral — you’ll encounter various loan types. One less common option is a balloon mortgage.

This guide explains what a balloon mortgage is, how it works, and what you should consider before choosing it.

What Is a Balloon Mortgage?

A balloon mortgage has regular monthly payments based on a long amortization schedule (like 30 years) — but the loan itself matures much earlier (often in 5, 7, or 10 years). At that maturity date, the remaining balance — the “balloon” — is due in full.

Example:

You take out a loan for $400,000 with a 30‑year amortization but a 7‑year balloon term.

After 7 years, the remaining balance must be paid off in a lump sum — either by selling, refinancing, or using savings.

How It Works

-

Monthly Payments: Often lower because they’re based on a long amortization schedule.

-

Balloon Due Date: A large final payment is due when the loan matures.

Why People Choose Balloon Mortgages

1. Lower Initial Payments

In the first years, payments are lower compared to a standard mortgage.

2. Short‑Term Ownership Plans

If you plan to sell a Miami Beach condo or a Coral Gables home within a few years, a balloon loan may work well.

3. Expecting Higher Income Later

Some buyers anticipate higher earnings or refinancing.

Risks of a Balloon Mortgage

1. Big Lump Sum Due

If you can’t refinance or sell, you may struggle to pay the final balloon payment.

2. Market Risks

In slower markets like sometimes seen in Little Havana or Overtown, selling before maturity might be harder.

3. Refinancing Depends on Approval

If your credit or market conditions change, refinancing may not be guaranteed.

Who Might Consider a Balloon Mortgage

A balloon mortgage may fit if:

-

You’re a real estate investor planning a short hold

-

You expect large income growth

-

You plan to renovate and flip a Coral Gables or Brickell property

But it’s not ideal for long‑term, indefinite homeownership without a solid exit strategy.

Conclusion: Balloon Mortgages for Strategic Buyers

A balloon mortgage can offer short‑term advantages for specific buyers in the Miami market. If you’re targeting Brickell condos, Coconut Grove homes, or Miami Beach properties with a short timeline, understand both the benefits and risks before committing.

Frequently Asked Questions (FAQs)

Can I refinance before the balloon payment?

Yes — many buyers refinance before the maturity date to avoid paying the lump sum.

Is a balloon mortgage risky?

It can be if you’re not confident you’ll sell or refinance before maturity.

Are balloon mortgages common in Miami?

They’re less common than traditional fixed or adjustable mortgages but used by some investors or short‑term buyers.

Categories

Recent Posts

GET MORE INFORMATION